The need for KYC and AML compliance has become mandatory to comply with the global and local regulations. Understanding AML vs. KYC can help you understand the difference between the two terms and implement these processes to ensure compliance.

The ones who fail to do so, are subjected to harsh regulatory penalties. To avoid fines, businesses should identify the underlying company standards and the need for KYC and AML compliance in the business framework.

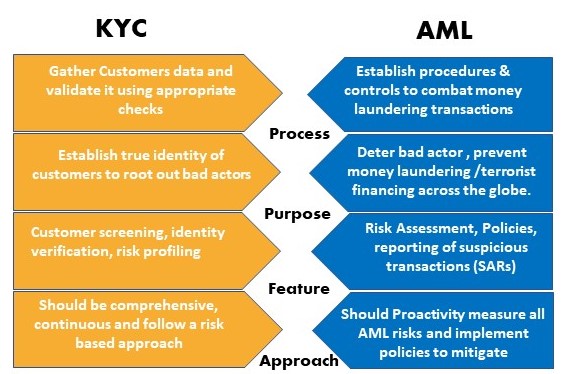

What is KYC?

KYC is the initial step in the implementation of a broader AML compliance process. It refers to understanding and figuring out the potential risks associated with a customer. This includes factors like verifying the customer’s identity and understanding their financial dealings to effectively manage risk. It’s a fundamental part of any AML programme.

Typical KYC process includes:

Verifying the customer’s identity to prevent fraud

Screening the customer against prohibited lists

Assessing the customer’s risk profile to determine if they’re higher risk

Ongoing monitoring, including transaction monitoring, to make sure their risk profile hasn’t changed

What is AML?

Anti-Money Laundering (AML) includes policies, laws, and regulations to prevent financial crimes. AML is a worldwide term to prevent money laundering. Global and local regulators are established worldwide to prevent financial crimes, and these regulators create AML policies.

Standard components of the AML Compliance Process includes:

KYC procedure incorporates Customer Due Diligence (CDD) & Enhanced Due Diligence(EDD).

Risk-based AML policies

Ongoing Risk Assessment and Ongoing Monitoring

AML compliance training programs for staff

Internal Controls and Internal Audits.

Key differences between KYC and AML

AML (anti-money laundering) is an umbrella term for the range of measures, controls, and processes that firms must put in place in order to achieve regulatory compliance. By contrast, KYC is a component part of AML, and refers specifically to the means by which firms establish and verify their customers’ identities, and monitor their financial behavior.

Alia Noor (FCMA, CIMA, MBA, GCC VAT Comp Dip, Oxford fintech programme, COSO Framework)

Associate Partner Ahmad Alagbari Chartered Accountants